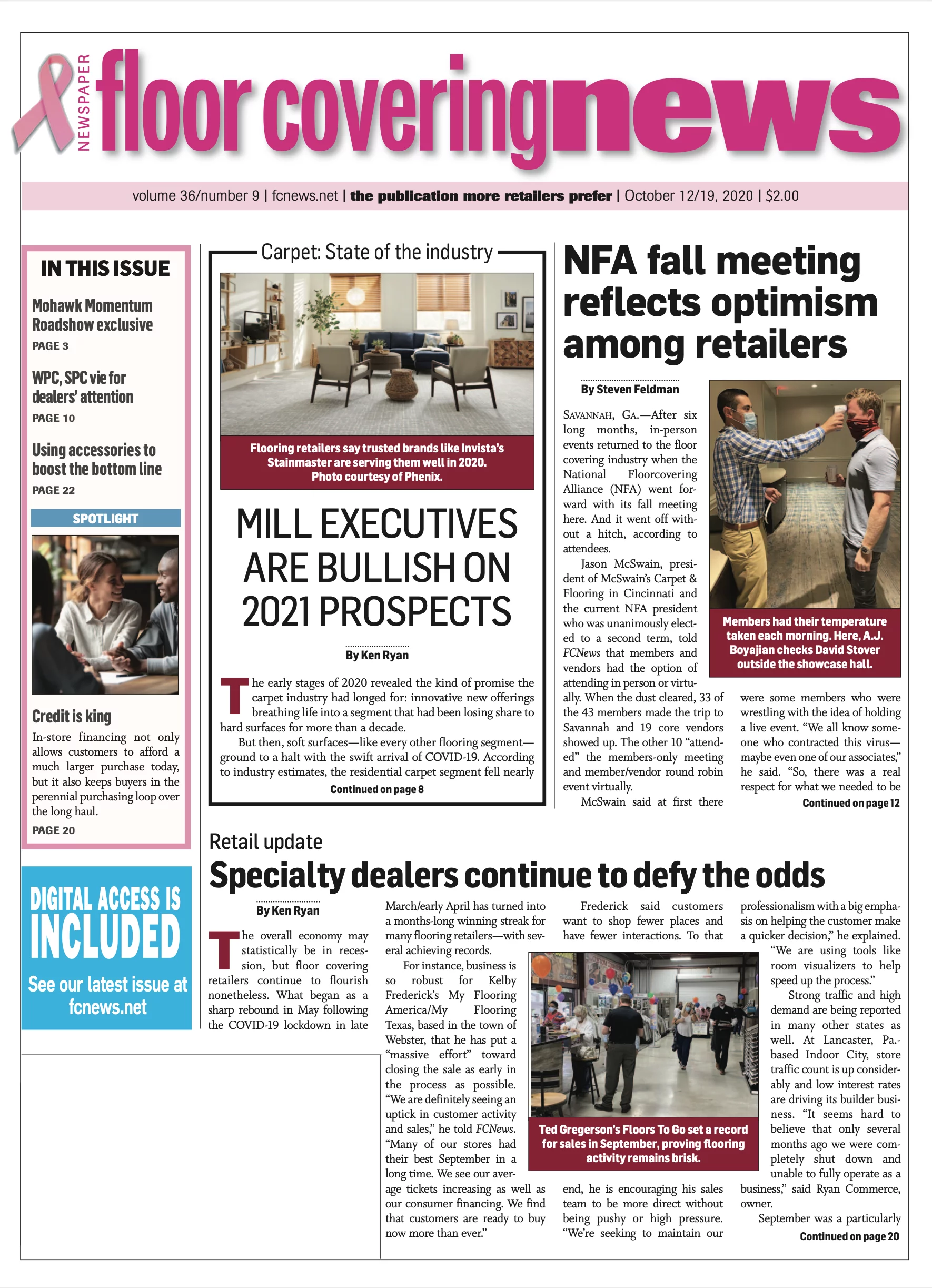

By Nicole Murray

One of the perks of offering in-store credit options is it allows customers to afford a much larger purchase—especially when they discover the floor remodel of their dreams was estimated to cost more than they anticipated. Another, slightly less well-known perk, experts say, is financing also keeps that customer in the “perennial purchasing loop” due to the credit history and relationship established with a retailer over the long term.

To the first point, purchases made utilizing these credit programs have been shown to be much larger—at times more than double—than the original amount she intended to spend when she walked through the door. “The average purchase with a branded credit card is around $4,000,” said Doug Ensley, senior director of residential marketing development at Mohawk. “On average, that is typically 47% more than the customer intended to spend.”

That spells opportunity for floor covering retailers looking to not only grow sales but also profits as an overall percentage of sales. On average, each ticket financed is more than three times higher than it would be if no financing was involved, experts say.

“In our most recent annual consumer purchase survey, Synchrony cardholders reported spending 54% more compared to general big-ticket shoppers,” said Sam Mudrick, relationship manager for Synchrony Financial. “In addition, 77% of Synchrony cardholders said they planned to use their credit card again in the future, which drives repeat business.”

Many retailers agree, adding that consumer financing opens up new avenues. “Flooring is an expensive purchase, and the consumer is put at ease when she has the option to pay off her purchases little by little vs. all at once,” said Billy Mahone, president of Atlas Floors Carpet One Floor & Home, San Antonio, Texas.

Credit also has the ability to alleviate potential “sticker shock” consumers might experience when they receive an estimate for the floor of their dreams—especially if they haven’t purchased flooring in a long time. “We have found most people don’t have $10K sitting in the bank,” said Steve Weisberg, president of Crest Flooring, Allentown, Pa. “There are so many other major purchases that are financed—cars, houses, etc. It just makes sense to have that option for flooring as well.”

Another benefit of credit is it allows the customer to either trade up to higher-end goods or add more rooms to the remodeling project. “Some will come into the store with a plan to first redo their kitchen, then their living room and then their bathroom,” Atlas Floors’ Mahone explained. “However, once she realizes how much financial flexibility there is when she has up to 18 months to pay everything off, she usually opts to do everything at once and with a better product.”

What’s more, many customers who are approved for a line of credit are usually given a larger amount than they expected, which opens the opportunity for additional rooms or trade-up products. “It becomes a prime opportunity to sell her as much as possible because we know the amount she has been given to work with, which will affect the products we show her,” said Keith Spano, president of Flooring America, Flooring Canada, International Design Guild and the Floor Trader. “The phrase, ‘We can’t afford that’ isn’t really uttered because she is thinking in terms of monthly payments, not the total lump sum.”

More importantly, customers who have a positive experience the first time around are much more likely to return for business in the future because their line of credit remains ready to use for upcoming projects. “The credit line can just sit there for a few years until they are ready to do another project,” Spano said. “They just have to walk in and say, ‘OK, it’s time,’ and we repeat the process without digging into her pocket.”

Cost of credit

Retailers who opt to take part in these credit programs can benefit because in many cases the credit card fee is already calculated into the cost of the job. “A typical credit card has a 2.5% rate and financing is less than that,” Spano explained. “It is a plus for everyone, because if you are paying less than what you would have if she uses a credit card, you are being given the tools to hold your margins and to keep everything affordable.”

What’s more, in many cases the retailer receives the entire sum from the financial institution almost immediately as opposed to only receiving a partial payment when the customer uses a credit card.

Credit programs, such as those offered by Synchrony Financial, offer a one-stop shop of online resources that retailers can use to educate staff and customers can use to research, apply and even pay her monthly fees online. “Our tailored programs engage customers when and where they shop,” Mudrick said.

For many customers, the key is the flexibility these credit programs provide. “If someone wants to pay a bit more one month to try and get ahead, or if they suddenly decide they want to pay the remaining balance, they can,” Mahone said.

Want to know how and when to promote financing to your customers? Check our industry tips that explain just that, here.